The Fiduciary Difference: Understanding Financial Advisors, Compensation Models, and Why it Matters

December 1, 2025

A fiduciary is legally and ethically obligated to always act in your best interest, even when doing so conflicts with their own interests. This should matter to you because it is a legally enforceable duty that reflects the highest standard of care in financial services and influences every recommendation, decision, and action.

The Portfolio Strategy Group is a fiduciary for every client and account, always. We believe that an unwavering fiduciary commitment is a critical differentiator among advisors. Without it, it can be confusing to know who truly prioritizes your best interests, and who may be putting their own first.

The Fiduciary Obligation: What This Means for You

The fiduciary standard requires an advisor to:

Put your needs first always.

Act with ongoing prudence, care, and diligence, tailoring carefully researched recommendations to your specific needs and circumstances.

Disclose and manage all potential conflicts of interest, including those related to compensation and product selection.

Avoid misleading statements or omissions that could cloud your judgment.

Honor your stated goals and instructions throughout your relationship.

Not All Advisors are Fiduciaries: The Suitability Standard in Contrast

Do not assume that your advisor is a fiduciary. Many large-firm (wirehouse) advisors are not fiduciaries and operate under a far less protective “suitability” standard.

Suitability requires that recommendations only be “suitable”– not necessarily optimal or in your best interest.

Advisors operating under this standard:

Can recommend higher-cost or less effective investments (that may generate more revenue for their firm).

Are not required to put your needs ahead of their own.

Can disclose conflicts yet still proceed with recommendations that benefit them.

May earn commissions or benefit from sales incentives that influence advice.

In 2020, Regulation Best Interest (“Reg BI”) added limited protections for investors but is still a lower standard than a continuous fiduciary duty, as it applies only when a recommendation is made, not ongoing.

No matter how honest they may be, a non-fiduciary advisor is not obligated to treat you with the highest standard of care.

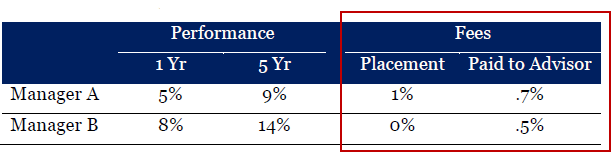

An Example:

Consider two managers with distinct performance histories and advisor compensation:

Manger A underperforms Manager B but pays the advisor more.

Manager B delivered higher returns with lower fees over 5 years.

Under suitability, both may be acceptable, allowing an advisor to choose A (even if B is better for the client). A fiduciary advisor must ignore sales-based compensation entirely and recommend the option that best serves the client (in this case, Manager B).

Over time, these fee and performance differences compound and can significantly impact an investor’s wealth.

Two Compensation Models: Understanding the Difference

Advisors typically earn revenue either through:

The Registered Investment Advisor (“RIA”) model

The traditional broker-dealer model

Some firms are a blend of both which creates confusion and requires clarity about when fiduciary obligations apply and when they don’t.

The Registered Investment Advisor (“RIA”) Model

RIAs are regulated with the Securities and Exchange Commission or a state securities regulator under the Investment Advisers Act of 1940, which has always mandated a continuous fiduciary standard.

RIA advisors generally:

Earn transparent, fee-based compensation (often a percentage of assets under management or a fee for time rendered).

Act as a fiduciary at all times, beyond the point of sale.

Access the full universe of investment managers.

Do not face sales quotas or corporate pressure to promote specific investment options.

Typically operate as independent firms (though there has been consolidation within RIAs).

Disclose conflicts in the Form ADV, which is publicly available online here.

The RIA structure naturally aligns advisor and client incentives for portfolio growth.

The Broker-Dealer Model

Large firms such as Morgan Stanley, JP Morgan, Bank of America Merrill Lynch, and their registered representatives operate primarily as broker-dealers, regulated by FINRA (Financial Industry Regulatory Authority). Their size and scale allows broad product offerings, many of which are proprietary and internally distributed.

Broker-dealer advisors may:

Be compensated through commissions or transaction-based fees.

Operate under the suitability (not fiduciary) standard.

Face incentives to recommend proprietary products, products with higher fees, or meet sales quotas.

Recommend only from a pre-approved list of investments.

What Can This Mean Over Time? The Fiduciary Advantage

Even small differences in cost, transparency, and investment objectivity can compound significantly over time:

Lower Costs:

Fiduciary advisors must consider an investment’s costs as well as benefits. Fiduciaries avoid hidden fees, unnecessary trading to generate commissions, and undisclosed revenue sharing that eats into returns.

Broad Investment Selection:

Fiduciaries may select investment options from the entire investment universe, not from a limited pre-set or internal menu. This process supports making recommendations that are solely in your best interest.

Ongoing Care:

Fiduciaries are required to continuously monitor, assess, and rebalance client portfolios to keep them aligned with your goals beyond the point of transaction.

Holistic Planning:

Most fiduciary advisors embrace comprehensive financial planning that considers your entire financial picture (investments, taxes, estate planning, retirement, etc.) to coordinate decisions across your entire financial life.

Behavioral Guidance:

Fiduciaries offer long-term perspective and investment discipline. This can be especially valuable during periods of market volatility to prevent costly emotional decisions.

Conflicts of Interest, Disclosure and Management:

Fiduciaries must eliminate conflicts where possible and fully disclose and manage those that cannot be eliminated with informed consent.

Accountability and Recourse:

The fiduciary standard provides a well-established legal framework for holding advisors accountable if they fail to uphold their duty.

Key Questions to Ask Any Advisor

Before partnering with an advisor, it’s essential to ask critical questions and clarify how they operate. As a fiduciary, some questions PSG is commonly asked by prospects are:

Are you a fiduciary 100% of the time? Will you put that commitment in writing? Some advisors claim to act as fiduciaries but qualify this with limitations. For example, they may act as fiduciaries only for retirement accounts.

How is your firm compensated and does the firm receive compensation beyond what I pay directly? Understand all revenue sources that could create conflicts (commissions, kickbacks, revenue sharing, etc.) and manage them accordingly.

Do you have conflicts of interest? How do you manage them? Every advisor has some conflicts. What matters is transparency and how conflicts are disclosed and managed. Do they require informed consent? Be cautious if an advisor claims no conflicts exist. Why take a chance to find out later there are conflicts you didn’t even know about?

What is your investment philosophy? Understand how advisors select investments for your account. You want to partner with someone who does the hard work to diligence and assess potential risks. You should know what drives investment recommendations.

Will you provide ongoing monitoring and proactive advice? Fiduciaries are obligated to continually monitor accounts. Confirm that the scope and frequency of ongoing service match your expectations.

Practical Steps for Investors

Clarify your needs: Determine if you need investment management, comprehensive financial planning, or both. Knowing what you need will help you identify the right partner.

Your assets, your name. Assets should be held in your name at a trusted custodian, not on your investment firm’s balance sheet.

Review credentials: Many advisors have earned advanced degrees or certificates (i.e., MBA, CFP®, CFA and CPWA® designations) to refine their expertise. Confirm relevant licenses (i.e., active Series 7, 63 for FINRA registered firms) and adherence to standards for each.

Verify registration and history: Leverage resources like BrokerCheck to ensure that your advisor and firm are properly registered and have not had any disciplinary actions.

Understand fees: Always know what you are paying and evaluate your performance net of all fees when possible.

Trust your instinct: A financial advisor is a trusted partner in managing your life’s savings and supporting your legacy. Choose a firm and a team who you trust, communicate, and feel compatible with.

RIAs in Summary

Independent RIAs such as The Portfolio Strategy Group offer something most wirehouses cannot: complete alignment with your interests. The fiduciary relationship is built on trust, transparency and a duty of care that endures throughout your financial life. These qualities transform a business relationship into a true partnership that should give you peace of mind knowing your assets are working for your future.

Have Questions?

Choosing the right partner means building a relationship with someone who stands behind you and your goals, giving you confidence that you are cared for through all market cycles.

At The Portfolio Strategy Group, fiduciary care is at the heart of everything we do and supports why we have become the family behind so many of our clients’ families.

We welcome the opportunity to guide you through the advisor selection process and help you make a decision that leaves you feeling supported, understood, and protected.

Let’s talk about your financial future. Give us a call today!

Important Disclosures: All opinions expressed in this article are for informational and educational purposes and constitute the judgment of the author(s) as of the date of the writing. These opinions are subject to change without notice and are not intended to provide specific advice or recommendations for any individual. PSG does not provide tax, legal or accounting advice, and nothing contained in these materials should be taken as such. To determine which investments may be appropriate for you, consult your wealth advisor prior to investing. As always please remember investing involves risk and possible loss of principal capital and past performance does not guarantee future returns.